Article Updated: January 7, 2023

Demand Letter Guide

Sample Letters for Settlement

This is your one stop shop for everything settlement demand letter related.

This is your one stop shop for everything settlement demand letter related.

To make your life easy, the entire article is hyperlinked, so you can pick out the parts you want to learn about, or read the whole thing, it’s up to you.

In this guide you will learn:

♦ What is an insurance demand letter

♦ How to write a demand letter

♦ How much to ask for in a settlement demand letter

♦ Whether/when to do a demand letter for policy limits

♦ What to include in a pain and suffering settlement letter

♦ What happens after your lawyer sends a demand letter

♦ Insurance demand letter response times

♦ Handling an adjuster’s failure to respond to demand letter

Despite practicing personal injury law for years (link to my bio), it took me a few days to summarize everything I know about demand letters and write this article. That said, if the article is missing what you’re looking for about preparing or handling a demand package for settlement, send me a message and I’ll update the article to include that missing piece.

Feel free to skip around the article, because the end of every chapter has a link that lets you jump back up to Table of Contents, which you can get to by scrolling below.

Chapter 1:

What is an Insurance Demand Letter

Demand Letter v. Demand Package

This Chapter will zip through two related, but different, topics. They are:

(1) what is an insurance demand letter

(2) what is a demand package in a personal injury case

Let’s tackle them in that order, starting with the first question.

Demand Letters for Insurance Claims

A bad driver that injures you in an accident owes you money, but how do you get it?

In most, but not all, personal injury claims, the lawyer will write a demand letter to the insurance company to get that money for you.

It would be nice if the other driver had a sort of security deposit in their insurance policy to cover your losses, but it doesn’t work that way. You have to wait for your recovery, and a demand letter is what gets the ball rolling with that process.

The purpose of the demand letter is an effort to settle your case without having to file a lawsuit. The insurance company will not pay any money on your case until it has its head wrapped around what your case is about. The demand letter gives the insurance company that knowledge.

It really is just what it sounds like – a letter, sent to the insurance company for the driver that caused your accident. If multiple other cars/drivers caused your accident, the letter would be sent to all of them.

I’ll get into the weeds of settlement demand letters later on, but the basic contents are: an outline of your accident, what your damages are, what you need to make the case go away and not sue.

Demand Package for Settlement

In lawyer talk, a “settlement demand” refers to your request for a specific amount of money to settle the case (i.e., “we will accept $150,000 to settle this case, that is our demand.”) This can happen before a lawsuit is filed or after.

In lawyer talk, a “settlement demand” refers to your request for a specific amount of money to settle the case (i.e., “we will accept $150,000 to settle this case, that is our demand.”) This can happen before a lawsuit is filed or after.

In contrast, in lawyer talk, the “demand package” is the written submission made to the insurance company inviting the insurance company to settle a case. This is almost exclusively done before a lawsuit is filed.

A demand package will include:

♦ Insurance demand letter

♦ Medical bills

♦ Photographs

♦ Medical records

♦ Police report

♦ Other injury/claim specific documents

Sometimes, with some insurance companies, it is a wasted effort to send them a demand package for settlement.

For example, State Farm has earned the nickname of “Snake Farm” amongst many lawyers, for refusing to honestly evaluate claims for its insured clients. Many lawyers will tell you that Snake Farm’s claim practices are so disingenuous that you are better off just filing a lawsuit and not wasting your energy preparing a demand package.

When to send a demand package, and for which scenarios, to which insurance companies, etc., is decided on a case by case basis which is something you should discuss with your lawyer.

If you’ve determined that you need to write a demand letter, which will be part of your demand package, continue to Chapter 2 learn how to write that letter. Or, return to the Table of Contents and jump to another Chapter to find what you’re looking for.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 2:

Demand Letter Writing Tips

Demand Letter Drafting Do’s & Don’ts

The focus of this section is on how to write a great car insurance demand letter, but this will serve as good information for any personal injury demand letter.

I will tell you the key 4 things you should do, and the key 4 things you should not do. Short list of 8 items, here we go…

Demand Letter Tip #1

Keep the Liability Story Short and Simple

Assuming the police report’s narrative is helpful for you, include a copy of the police report and use that description in your demand letter.

Do NOT add any more to that description. Remember, anything you say can and will be used against you. If your case does not settle, and you wrote your own demand letter, you can (in limited circumstances in under specific scenarios) be cross-examined and impeached on your summary of the accident in that letter. The phrasing you used to describe the accident can be craftily used by an insurance lawyer to kill your case.

If the police report’s narrative of how the accident happened does not help you, read our article on police reports and give serious thought to hiring an attorney, because your demand letter will, with 99% certainty, not get you a settlement worth accepting.

Demand Letter Tip #2

Highlight Your Property Damage

Highlight your property damage, which includes attaching a copy of the repair estimate report for your vehicle. You should also note if your airbags went off – although this is not substantively important, adjuster’s seem to think it is, so you’ll want to make mention of this if it happened.

Demand Letter Tip #3

Outline Your Medical Expenses

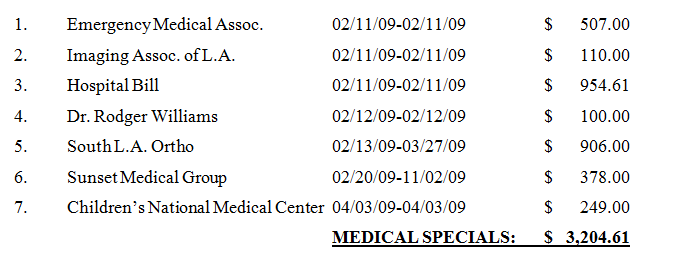

If you’re going to do this, do it right. That means you must go through each and every one of your medical bills, tally them up, and include a summary of them in your settlement demand letter. It will, hypothetically, look like this:

Demand Letter Tip #4

Limit Use of Descriptive Adjectives

When you start throwing around excessively exaggerated adjectives and descriptions (e.g., “terrified,” “pain is killing me,” “worst thing ever”), you lose credibility with the adjuster, and your valuation of non-economic damages goes out the window.

Let the facts tell the story, not you. This means fill your demand letter with all the facts that help your case, and that increase your case value. You will not get more money by crying in the letter, so avoid that.

Demand Letter Tip #5

Do NOT Set a Response Deadline

You may be tempted to set a response deadline, and tell the insurance company you will file a lawsuit if you don’t get a response by that deadline. Do not do this, it is a terrible idea for so many reasons.

For one, the adjuster can be busy or behind, and will not take kindly to you setting a superficial response deadline.

Also, if you’re writing your own demand letter that means you do not have an attorney. Your bark has no bite when you set a deadline for the adjuster.

Lastly, if you set a deadline the adjuster could think you are desperate for fast cash, and that could entice the adjuster to work slow and flush out how bad your position really is.

Long story short, do not set a respond deadline.

Demand Letter Tip #6

Do NOT Request a Specific Dollar Amount

It takes years, and hundreds of cases, to understand case values in personal injury cases and calculating their worth. Kindly put, you do not know how much your case is worth.

Knowing that, I hope you agree you should not speak first during this negotiation (rule of thumb, whoever speaks first loses in a negotiation). Let the insurance adjuster speak first and make an offer. Even if it’s a lowball offer, that’s the starting point from where you should be working, not a random number that you “think” your injuries and case are worth.

Work from the adjuster’s starting number, and build your way up by justifying why your case is worth more. This is a much better approach than guessing a number that is way off, and way too much, which will thwart meaningful negotiations.

Demand Letter Tip #7

Keep a Friendly Tone

It is recommended that you do not threaten or disparage the other party. Only appropriate language should be employed in the letter, ensuring it does not convey any anger or frustration. By creating a negative mood, you will only lessen the chances of reaching a fair settlement. Maintain an objective and professional tone in the letter, regardless of how frustrated you are with the situation.

Demand Letter Tip #8

Do NOT Include a Pain & Suffering Statement

Insurance companies are not what they used to be. Back in the day, insurance adjuster’s would use their human brain to evaluate your claim. Not so much anymore.

Now, a computer brain uses an algorithm to compute the settlement range of your case (e.g., between $30,000 and $40,000). That range is based almost entirely off your medical records, including CPT and diagnostic codes.

These computer algorithms don’t care about your “pain”, so do not waste your energy writing an essay about what the accident did to your life.

There is another, strategic, reason for holding back this information, which I discuss further down in this article. Keep reading to discover how to use this to your benefit, or return to the Table of Contents.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 3:

How Much to Ask For in a Settlement Letter

How Much to Ask for in a Personal Injury Settlement Letter

Earlier in this article you learned there is an attorney lingo for this (how much to ask for) called a “demand.” When you ask for money as an injured plaintiff, you are “making a demand” or “demanding” a certain amount of money.

It sounds aggressive, but it is not. It is the customary lingo and the insurance company will not be offended by you using this lingo.

Let’s use that proper lingo to explain this topic. You are likely to end up in 3 categories:

♦ Demand too little

♦ Demand too much

♦ Demand the correct value of the case

All of these are bad for, irrespective of the size of the insurance policy, and I will explain why.

Determine Size of the Insurance

As a precursor to writing a demand, you should try to find out the size of the insurance policy for the bad-driver. This isn’t always possible, but you should try.

Some states have a statute that compels the insurance company to disclose the size of the insurance policy. In those states, simply follow the statute.

For states that do not have that requirement, you can sometimes flush out the size of the insurance with some fancy footwork in speaking with the adjuster.

For states like California, where you are not statutorily entitled to know the size of the insurance for the other driver, the below advice regarding how much money to ask for is even more important.

Demand Letter Asks for Too Little

This is straightforward – you do not know how much your case is worth, or the real value range of your case, so you might end up demanding too little. What do you think the adjuster will do?

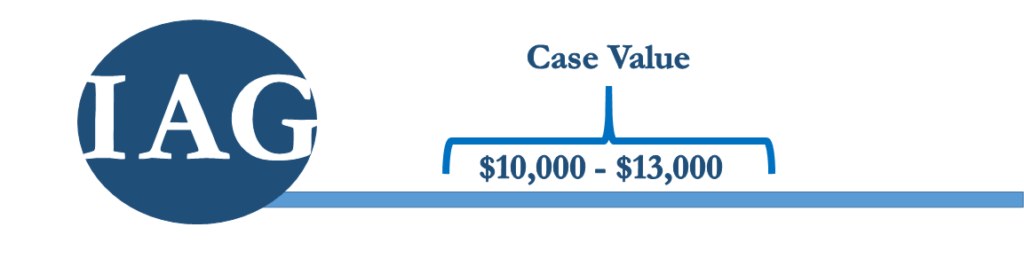

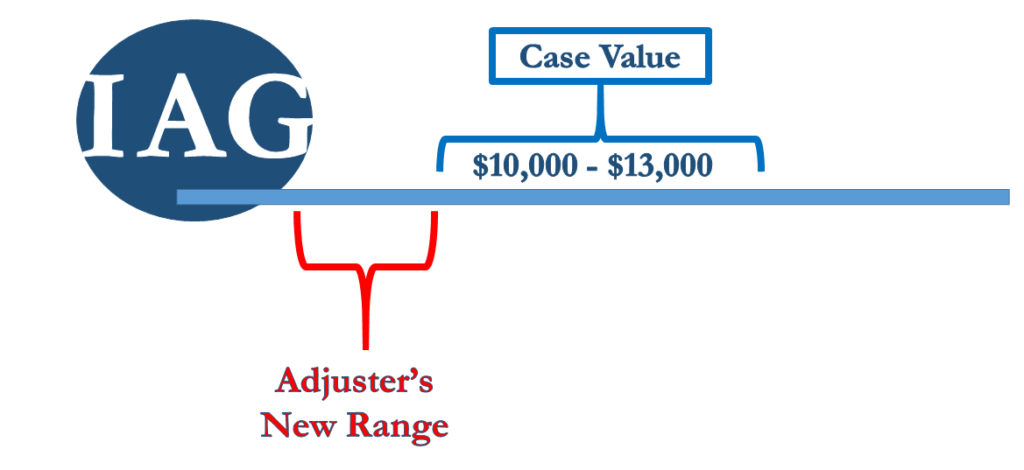

Let’s answer with some illustrations, assuming your case is worth between $10,000 to $13,000:

You demand $9,000 from the adjuster (which is too little if your case value is 10-13k).

A reasonable person might expect the adjuster to be ecstatic, because you demanded the bottom of the value range, and to immediately accept this demand and settle the case. That will not happen.

This is what the adjuster will do:

The adjuster will treat your starting number of $9,000 as the “top” of your settlement demand range, and reset the negotiation values to get you lower.

If this happens, you have dug yourself into a hole that you can’t dig out of without filing a lawsuit, or accepting an unfair settlement.

Demand Letter Asks for Too Much

You are not much better off if you ask for too much. If you ask for too much, the insurance adjuster (who negotiations hundreds of settlements yearly and knows the value of your claim) sees this and immediately knows that you do not know what you are doing.

Once the adjuster sees this, the adjuster will reasonably conclude that you are throwing up a big number to play high/low tug of war. Adjusters are use to this trick and it will not work, especially for a non-attorney.

The adjuster will dig in low and watch the clock burn away on your statute of limitations, putting your back up against a wall.

And that leaves us with option 3, an accurate value demand.

Demand Letter Asks for a Fair Settlement Amount

If in writing your demand letter you ask for a fair settlement, the insurance company and adjuster will against screw you the same way they would if you asked for too little.

If your case is worth between $10,000 to $15,000, you want to do everything in your power to get the $15,000. A fair settlement amount would be $15,000+. But if you make a settlement demand for $15k, you will never get that.

Again, the adjuster will consider that to be the top of your range, and pull you down from there.

Couldn’t you just start and end at $15k, and make that a take it or leave it? If you magically guessed a value within the fair range, that will get the deal done, right? Wrong.

The reason is the psychological mechanics of negotiations, especially with low-level negotiators like pre-litigation vehicle accident insurance adjusters. Your sturdiness at the fair value and refusal to “move” will come across as unreasonableness in negotiations.

Keep in mind, there are more than numbers at play here. There is an art to this, a very gentle art of persuasion. If you are not willing, or able, to play the game, then you should not be negotiating your own settlement. If you are not negotiating your own settlement, you should not be writing your own settlement demand letter.

How Much Settlement to Ask For in a Demand Letter

Your only choice is this: do not make a monetary demand. Leave it as a blank check, and invite the insurance adjuster to contact you with an offer. Use that as the starting point, and work your way up.

You are much more likely to end up in a better place if you use that approach (as a vehicle accident negotiator with little to no experience in this field) than using the approach of guessing wrong.

The only alternate approach to that is hiring an experienced negotiator to handle this with the insurance company for you. If you decide to take that route, our contact information is below.

Personal Injury Demand Letter for Policy Limits

There are always exceptions to the rules. Sometimes, your case demands the full policy, and there is no point dancing around that bush. If you are in that situation, you should come right out the gates and send a demand letter for policy limits.

When should you demand policy limits?

There is no logical rule for attorneys, it is situational.

If I had a gun to my head and had to make up a fake rule for non-attorneys, I would say if your medical expenses are 75% of the policy limits, then you should send a policy limit demand letter.

Read that again – I said if I had a gun to my head – so do not email me asking, “what if my medical expenses are 60% of the policy limits, should I send a policy limits demand letter?”

You might be looking at $15k policy limits, and have $10k in medical bills, but not have a policy limits case. I need to deep dive into your case for a real answer, one that’s worth it’s weight in gold. Without that deep dive, the made-up 75% rule is the only methodology I can offer.

Policy Limits Demand Letter Sample California

We have a unique challenge in California because it’s not easy to find out what the policy limits are before we file a lawsuit. We are stuck shooting in the dark.

What we do know is that the minimum policy limits in California is $15,000. That does not help us much though, because if we assume the policy limits are $15k but it is $30k in your specific accident, then we have only demanded 1/2 the policy limits and never in fact made a policy limits demand.

In my view, the best way to deal with this is through the following, California specific, policy limits demand letter sample:

Dear Mr. Adjuster:

My client was in a substantial accident with your insured, _________. The medical expenses alone are substantial, totaling $___________, and may justify a policy limits resolution to this claim.

Pursuant to Boicourt v. Amex Ins. Co. (2000) 78 Cal.App.4th 1390, I request that you disclose the policy limits so that we may assess the viability of this claim for early and immediate resolution without further inconvenience to the involved parties.

I look forward to your response, and thank you in advance for your prompt attention to this matter.

As you can tell from the case citation, this is a California sample, and won’t be relevant to any other state.

Demand Letter Sample for Wrongful Death

If you have a wrongful death case, you should almost always be making a policy limits demand.

Regardless of the size of the insurance, no policy can adequately reimburse the taking of a human life. For that reason, again, wrongful death cases must – without exception – be pursued with a full policy limits demand letter.

This is true even if it’s a tractor trailer case. They only have $750,000 to $1,000,000 policies, and we can all hopefully agree a human life is worth more than that.

The tricky part about wrongful death policy demands is proving the survival action and the wrongful death action. The former requires much more savvy, and if you don’t build that up correctly you could be leaving an extra million dollars on the table.

All that said, if the case is one for wrongful death, come out the gates and say that in the demand letter, and have as exhibits and attachments the death certificate and other supporting documents which prove it’s a death case.

Policy Limit Demand Letter Tips

Before you settle for the policy limit and resolve your claim, you must do a few things:

♦ Make sure other driver does not have excess insurance coverage

♦ Make other driver sign an affidavit of assets

♦ Confirm other driver does not have another applicable policy

What language should be included in the affidavit, and how you confirm excess coverage and other issues, will vary from state to state and situation to situation.

We have templates, but those only serve as the foundation. We tweak those templates based on the specific scenario in each case.

The bottom line is, do not settle for the policy limit until you complete the above marks, otherwise you could be precluded from making a later claim for additional insurance money that was available.

Next up is dealing with pain and suffering in a demand letter. Keep scrolling for that Chapter, or return to the Table of Contents.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 4:

Dealing with Pain & Suffering in a Settlement Demand Letter

Pain & Suffering Demand Letter

How to write a demand letter for pain and suffering is very tricky, because it comes with a substantial risk. You will learn that risk, and how to hedge against that risk, in this Chapter.

Car Accident Impact Statement

A car accident impact statement, sometimes called an injury impact statement, is an exhibit (a separate document) that is attached to your demand letter and included as part of the settlement demand package that you send to the insurance adjuster to begin negotiations to settle your claim.

Your medical bills and lost wages will be mathematically outlined in the demand letter. Your car accident impact statement attempts to non-mathematically outline your:

♦ pain

♦ suffering

♦ inconvenience

♦ hardship

♦ pre-impact fright

♦ mental anguish

♦ other non-economic damages

Now that you know what it is, let’s discuss the risk of including this in your settlement demand letter and how to hedge against that risk.

Car Accident Impact Statement Risks

I will use a classic example of how I have seen many clients hurt their cases to explain the risk of these impact statements.

You write for the insurance adjuster the following, in your pain and suffering impact statement:

“I can’t mow my lawn anymore, and getting out of my convertible is impossible now.”

The insurance adjuster does some digging around, and finds pictures of you after the accident mowing your lawn. The adjuster will heavily lowball you now, and you will never get a fair settlement.

The problem is, you did not literally mean that you are “unable” to mow your lawn. You meant that you cannot mow it the same, or as well, or that it takes you 3 sessions to do it, or 3 times as long. But your words, taken literally, read something else.

I spend hours reviewing these accident impact statements to make sure clients do not shoot themselves in the foot due to ambiguous verbiage that can be taken out of context or used against them.

In the absence of a skilled lawyer to help you, I offer the following solution.

Eliminating Car Accident Impact Statements Risks

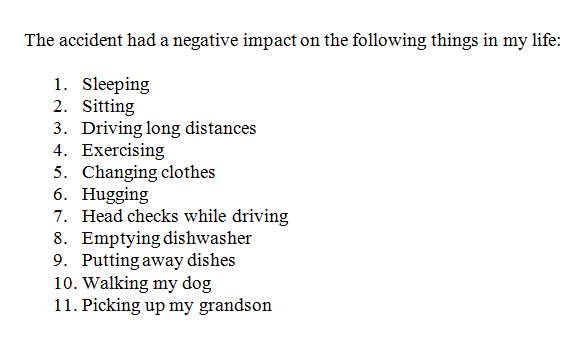

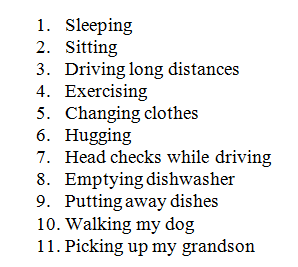

Most clients show me paragraphs and pages of summaries wherein they outline their pain and suffering related to their accident. That document is a goldmine for cross-examination and will likely do you more harm than good.

Without a lawyer, here is the best injury impact statement example I can offer you:

That victim impact statement example works for any car accident, limits your exposure to being impeached, yet gives the adjuster a forest for the trees view of your accident pain and suffering.

That victim impact statement example works for any car accident, limits your exposure to being impeached, yet gives the adjuster a forest for the trees view of your accident pain and suffering.

When you get on the phone with the adjuster (I cringe envisioning you speaking with an adjuster without an attorney to protect you, and that’s another story, but please read this article about when to hire an attorney), you can then orally explain more about each pain and suffering element to ensure it is placed in proper context.

Pain & Suffering Witnesses

Another idea is to get similar lists or short summary statements from family members. Family members are a great source of evidence for pain and suffering. Besides, who knows you better than your mom, dad, son, daughter, wife, husband or other close family?

When getting impact statements from family, the same words of caution apply. Don’t get too detailed because then your family may become a vulnerability in your case evidence, not a strength.

Also, it’s a good idea to not identify the family members, otherwise, you are giving up too much too early. There is a proper way to do this generically that an attorney can help you accomplish.

Short Pain & Suffering Statement Benefits

For novice car accident negotiators like yourself, holding back the full details of your pain and suffering information is helpful in another way.

When you have your first call with the insurance adjuster, you’ll have some additional information (about your pain and suffering) in your back pocket that you can bring up and use to move the needle in negotiations.

For all these reasons, my suggestion is to hold back your detailed pain and suffering impact statement examples until your first call with the insurance adjuster.

Keep reading to learn what happens after your demand letter goes out, including response times, or return to the Table of Contents.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 5:

Demand Letter Timeline & Response Time

Next Step After Letter of Demand

After a demand letter is sent what happens next? In this Chapter, you will learn the ins and outs of what happens after your lawyer sends your demand letter.

Demand Letter Timeline

Let’s start with the demand letter timeline. The timeline does not even begin until you are 100% done with all of your medical treatment. For that reason, it is impossible for anyone to predict the full demand letter timeline for you because nobody can predict how long your injury recovery treatment will take.

Once your treatment is done, however, your demand letter timeline will include the following stages:

♦ Collect all outstanding medical bills and records

♦ Sort and organize all medical bills and records

♦ Prepare and mail settlement demand package

♦ Following up with insurance company and adjuster

♦ Negotiate and finalize settlement or file a lawsuit

♦ Distribute settlement money to client

After your lawyer sends a demand letter, you can see the next step is following up with the insurance adjuster to start the settlement negotiations.

How Long Does an Insurance Adjuster Have to Respond to a Demand

Which brings us to this, how long does the insurance adjuster have to respond to your demand before your lawyer should start bugging the adjuster?

There is no set amount of time for this. The best response is two fold, which I’ll outline for you.

First, there are a lot of variables at play, including how lazy the adjuster is, how busy the adjuster is, how many cases the adjuster is being forced to handle, how complex your demand is, and how voluminous your demand package is, to name a few.

On average, for car accident claims, it typically takes insurance adjusters two months (60 days) to respond to a demand package and settlement demand.

Second, there is the psychological negotiation aspect of this, which is, if you start following up with the adjuster you are screaming that you are desperate for money and/or desperate to settle.

If you are desperate for money, then be prepared to take a serious discount on the real value of your case, and you can follow up 30 days after the demand package is mailed.

If you are not desperate, patience is a virtue, hang tight, and the adjuster will get back to you in 60-90 days on average.

Unless there is a statute of limitations deadline pressing me, I would wait 90 days before following up with the adjuster. While the insurance adjuster has, in some respects, as long as she/he wants to respond to your demand package, I would say this represents the far end of the limit and at the 90 day mark a gentle follow-up is in order.

The one thing you can, for an adjuster to receive a demand letter timely, is send it via FedEx or certified mail. At least that way you won’t waste weeks or months wondering if they even got it. This helps because it prevents you from having to follow up – and sound desperate – just to ask nervously if the adjuster received your demand letter.

No Response to Demand Letter What to Do Next

This is covered in the prior section, but to recap:

♦ The average adjuster response time to a settlement demand is 60 days

♦ If the adjuster has not responded by 90 days, you should follow-up

Thus, if there is no response to your demand letter, what should you do next? Follow-up, very gently, with the adjuster.

What do I mean by very gently? Your first follow-up should simply ask for confirmation that the adjuster received your settlement demand package. Nothing more, nothing less.

You can slowly notch it up in terms of inquisitiveness, but your follow-ups should always stick to confirmations and asking for timelines. For example:

“I had an automatic reminder on my calendar to check in on your review of the demand package in this case, please let me know where you are when you get a chance.“

Complete Failure to Respond to Demand Letter

If you waited 90 days, gently followed up one time, then did another 1-2 follow-ups but have never gotten a response, you are facing a rare failure to respond to demand letter situation.

You have two choices if the adjuster fails to respond to your demand letter, effectively ignoring it and you:

- Call the insurance company and ask for a supervisor

- File a lawsuit

In all my experience, I can tell you this with certainty, you will want to file a lawsuit 99.99% of the time. Why?

You just called the adjuster’s supervisor and got the adjuster in trouble. Do you really think that adjuster is going to do you any favors or offer the top value within that adjuster’s settlement authority? ABSOLUTELY NOT!

What I would do in this situation is file a lawsuit. A different, litigation adjuster, will often get assigned to the file. That adjuster, or the insurance company’s lawyer, will eventually reach out to you. At that point I would tell that person:

“the only reason I filed suit is because the pre-litigation adjuster was not responding to my demand letter or follow-ups, do you think we can settle this case or should we proceed with discovery and depositions?“

Some cases will settle with this approach, some will not. Regardless, it is a part of my arsenal that I have on standby to use for my clients to short circuit litigation and quickly get cases resolved and put money in their pockets.

Next up, a sample personal injury demand letter. Alternatively, return to the Table of Contents.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 6:

Demand Letter Sample for Personal injury

Demand Letter Sample : Auto

I will provide you with a nice copy/paste template here that is free for use. For the most part, you can plug in your case specific details and use this as the framework for any personal injury demand letter.

Sample Personal Injury Demand Letter

John Do

1234 Main Street

Los Angeles, CA 12345

February 6th, 2021

ABC Insurance Company

123 High Street, Suite 20

New York, NY 12222

Your Insured: David Wood

Claimant Name: Sally Sue

Claimant DOB: 1/1/2001

Claim Number: 123456

Re: Vehicle Collision of 1/1/2020

Dear Mr. Adjuster:

Please accept this demand package with respect to the above referenced claim number, offered to facilitate mutual resolution of this matter without the need for litigation.

This claim concerns a car accident that happened on _________. Generally, as outlined in the police report, attached hereto, the following occurred during the subject accident: ______________________________.

Photographs of the involved vehicles are provided with this demand. A property damage estimate is also enclosed. The estimate notes the following significant damage to my vehicle: _________________________________.

A copy of my medical bills are attached. A summary of the medical bills is as follows, and shows the following economic damages:

My medical records are also attached. Significantly, the records note the following, amongst other, injuries and conditions caused by this accident: ___________________________________________________.

In addition to the foregoing economic damages, I suffered non-economic damages. In the interest of brevity, I summarize those damages as follows:

Due to the accident, I also missed time from work. Attached is a work slip from my supervisor, and also a doctor’s note recommending that I rest for the periods of time that I did not work. My lost wages for this time period total $____________.

Please find all the foregoing evidence, witness statements, police reports, bills, employer statements, and the photographs attached with this letter. If you require additional facts or documents to fairly evaluate this claim, I invite requests for same.

I look forward to receiving your reply and working with you to resolve this matter.

Regards,

Ray Benjamin, Esq.

Enclosures

Demand Letter Sample : Product Liability

August 10, 2010

DEFENDANT

C/O Corporation Service Company

Suite 400

2711 Centerville Road

Wilmington, DE 19808

Re: Pennsylvania Facility

Dear DEFENDANT:

My office represents PLAINTIFF with respect to its purchase of DEFENDANT’s 30-Ton Cyber Grow Units (the “Units”). DEFENDANT and its Units caused over $15,000,000.00 of economic damages to PLAINTIFF. As outlined below, the DEFENDANT Units are not capable of controlling humidity, have a material defect which limits their functionality, and DEFENDANT’s representations about the Units are false and misleading. I write in an effort to resolve PLAINTIFF’s claims related to this loss amicably and without the need for protracted litigation or evidence of the DEFENDANT Units’ failures to be publicized throughout the flower community.

DEFENDANT was not in the business of flower cultivation. It was a traditional HVAC company with a focus towards HVAC systems for data rooms. In 2014, DEFENDANT saw an opportunity for additional profit by modifying its data center units and marketing them for use in the growing flower industry. To give the impression it made flower specific HVAC units, DEFENDANT went so far as to photo-shop images of flower plants onto its data room HVAC systems in its digital marketing materials.

To break into the flower market, DEFENDANT misrepresented and exaggerated the usefulness of its Units through numerous marketing materials, including PowerPoints, research papers, and marketing literature. In these publications, DEFENDANT admitted it knew flower plants are susceptible to damage if exposed to humidity (“RH”) at high levels, and in particular that flower plants in the bloom/flower stage of growth cannot safety endure RH higher than 50%. (Ex. 1 pg .5.) Further, DEFENDANT’s Director of Technology has admitted in marketing materials that flower plants continue to need RH control during their lights out cycles, when the lights in the grow room are turned off.

PLAINTIFF visited the DEFENDANT facility. DEFENDANT made misrepresentations to PLAINTIFF consistent with those in its marketing materials. Namely, that the DEFENDANT units can adequately control RH in flower grow rooms. In addition, DEFENDANT concealed, both in person and in its marketing materials, the fact that the RH control feature of its Units do not function unless the cooling feature is activated. Had PLAINTIFF known of this material fact, it would never have purchased the DEFENDANT Units. This limitation causes the need for additional reheat which offsets the alleged, touted benefits of the DEFENDANT Units.

Based on DEFENDANT’s misrepresentations and concealment of material facts about the abilities and limitations of its Units, PLAINTIFF was deceived into purchasing $1,400,000.00 worth of the Units for its Pennsylvania facility (the “Facility”). (Ex. 2.) Delivery of the Units to PLAINTIFF began in April of 2010, with startup continuing through June of 2010.

DEFENDANT’s direct interactions with and misrepresentations to PLAINTIFF give rise to contractual and tort causes of action. DEFENDANT’s concealment of material facts also opens the door to fraudulent concealment and punitive damages claims. I am confident discovery will reveal additional findings about what DEFENDANT knew about its Units and their functionality, or lack thereof, when it sold those Units to businesses across the country. I am also confident that knowledge of this litigation throughout the flower community will result in other victims of DEFENDANT’s Units coming forward.

Please forward this correspondence to your legal department and liability insurance carrier(s) as a potential claim. Failure to notify your liability carrier may result in denial of the claim and result in DEFENDANT paying out of pocket for defense and litigation costs related to this forthcoming litigation. Kindly have the appropriate representative contact me for settlement discussions related to this claim.

Sincerely,

Ray Benyamin, Esq.

Demand Letter Sample in California : Automated Submissions

Alternatively, the California Judiciary offers a form generating template on their website to help you prepare a demand letter.

I would never advise that anyone use this unless it is for a small claim, and relates to a contract or transactional matter. Nonetheless, it is there for you should you decide to use it.

I wrap the article up with closing thoughts below, or you can return to the Table of Contents.

The Finish Line

Demand Letter Help

Either you’ve read this article and are excited to write, send, follow-up on, and negotiate your own settlement demand letter to the insurance company, or you realized you’re not comfortable investing the time and emotional capital needed to do this.

If you’re in the former group, I’m glad this article gave you that confidence. Happy hunting!

If you’re in the latter group, that’s what I’m here for. I invite you to call me, a dedicated Los Angeles personal injury lawyer, who can take this stress off your shoulders and fight the insurance company for you.

All personal injury lawyers are not the same. Find out how we are different. You can reach out 24/7 at (800) 484-0779, e-mail me at info@injuryag.com, or fill out the contact form below.

If you skipped any sections and want to return to them, go to the Table of Contents.

About the Author

Article Author: This law article was written by attorney Ray Benyamin, Esquire. Mr. Benyamin received his Juris Doctor degree from the Thomas Jefferson School of Law, and his license to practice law from the State Bar of California. His law license number is 277263. He has been practicing law for 10 years. Mr. Benyamin is a registered member of the following legal organizations: Consumer Attorneys Association of Los Angeles (CAALA), the Los Angeles County Bar Association (LACBA), the State Bar of California, the American Bar Association (ABA), and the American Association for Justice (AAJ). Mr. Benyamin has personally helped his clients recover over $10,000,000 in vehicle accident insurance claims in the State of California.

![]()