Article Updated: December 7, 2021

Accident Medical Bills 101:

A Walk-through of:

Who Pays Medical Bills in a Car Accident

A Distinction With a Difference

There are two different questions on this topic, with two different answers:

♦ First: who pays your medical bills after a car accident? Depending on how your lawyer handles your claim, and when you retained a lawyer, the answer will be some variation of you, the other driver that hit you, and nobody.

♦ Second: who should pay your medical bills after a car accident? Assuming another driver is at fault, that driver or that driver’s car insurance company, should pay your post-accident medical bills.

This is NOT semantics. This is a distinction with a substantial difference.

Just because someone else is at fault does not mean they will pay your post accident medical bills. Here are just a few situations where the at fault party may not pay some, or all, of your medical bills after a car accident:

♦ You go to trial and lose on liability

♦ The insurance company claims some or all of your bills are for medical treatment not caused by your car accident

♦ The insurance company claims some or all of your medical charges are excessive, and only offers to pay a portion of them

Not an exhaustive list, but you get the point.

Normally, When in a Car Accident Who Pays the Medical Bills?

By “normally” I mean a perfect world, where the insurance company and insurance adjuster do not play games, and we apply the law to your case without hiccups.

In such a scenario, the law allows you to recover your medical expenses that were incurred because of your car accident from the person who caused your accident. If that person had car insurance, her or his car insurance company would pay your medical bills after your car accident.

However, that generic response does not fully answer your question. Why?

That generic answer fails to consider the issues of medical liens, subrogation rights, health insurance, recoverable charges and payment schedules, and how those issues create a “net result” of who pays how much of your medical bills after a car accident. This article covers all of that.

99.99% Likelihood This Information Applies to Your Case

Who will benefit from reading this article? Anyone who was in a vehicle accident, received medical care, and any of those medical bills were paid by:

♦ Private health insurance

♦ Employer health insurance

♦ Medicare

♦ Medi-Cal

♦ Medicaid

♦ Tricare

♦ No health insurance and attorney referred medical treatment on lien

That is 99.99% of car accident victims. The only people this article will not apply to are those who pay 100% of their medical bills out of pocket.

Enough background, let’s get started and learn the 101’s of who pays whose medical bills in a car accident.

Chapter 1:

Subrogation Rights for Accident Medical Bills

Medical Bills After a Car Accident Are

Paid Back, Partly, Through Subrogation

Your medical bills incurred after and as a result of a car accident are paid back, in part, through subrogation rights of a health insurance or payment provider, such as Medicaid, Medicare, or Blue Cross Blue Shield.

I will explain this in the following 4 steps:

1: Introduce sample fact patter to help you visualize accident medical bill payment obligations

2: Explain how car accident medical bills are paid when there is private or government health insurance

3: Explain from where and how subrogation rights attach to your post accident medical bills

4 – Map out the net result of the medical bill obligations of you and the negligent driver after subrogation rights are applied

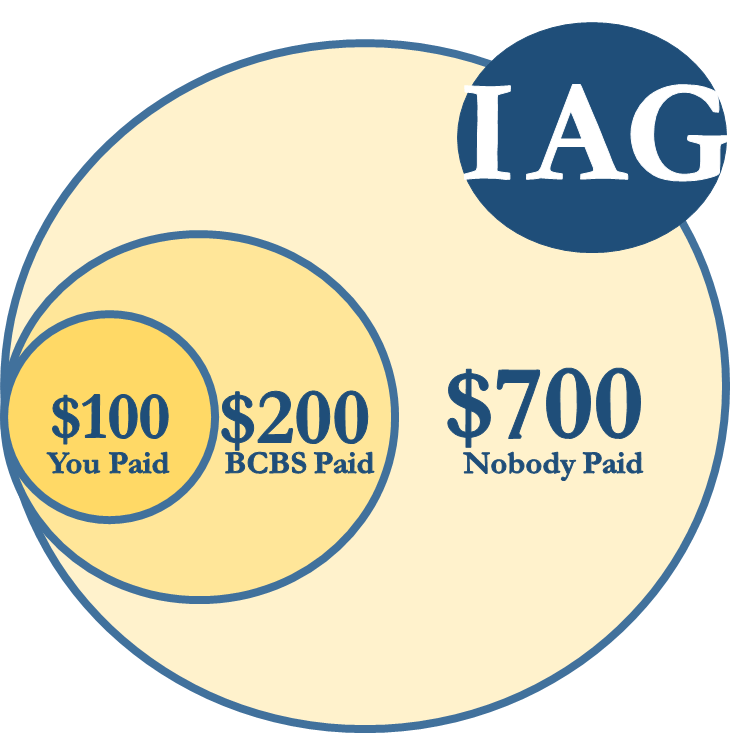

We will begin with a very simple hypothetical for a $1,000 medical bill.

1: Sample Car Accident Facts

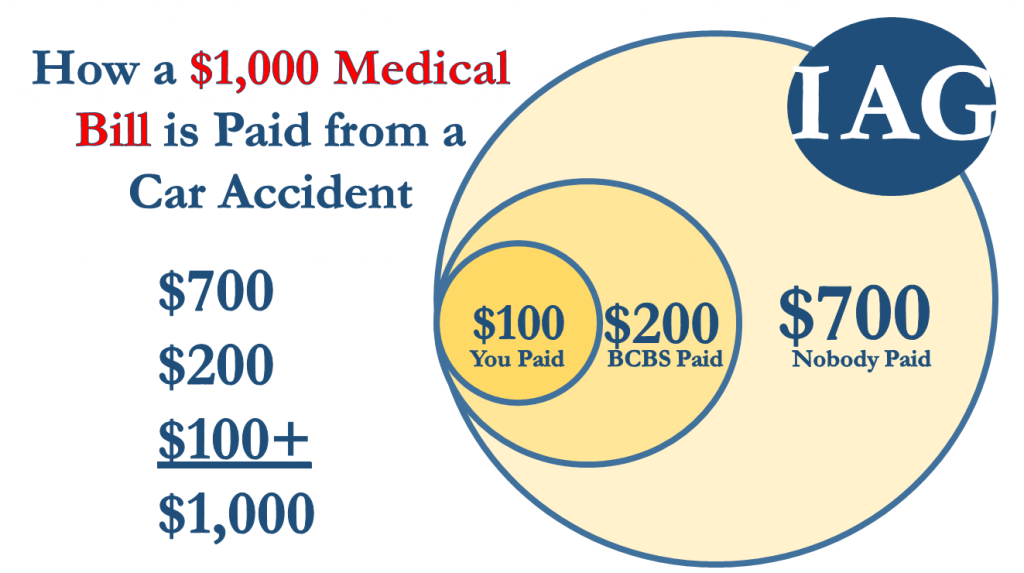

Using numbers will make this easier to discuss and understand. For the rest of this Chapter, we will use this hypothetical:

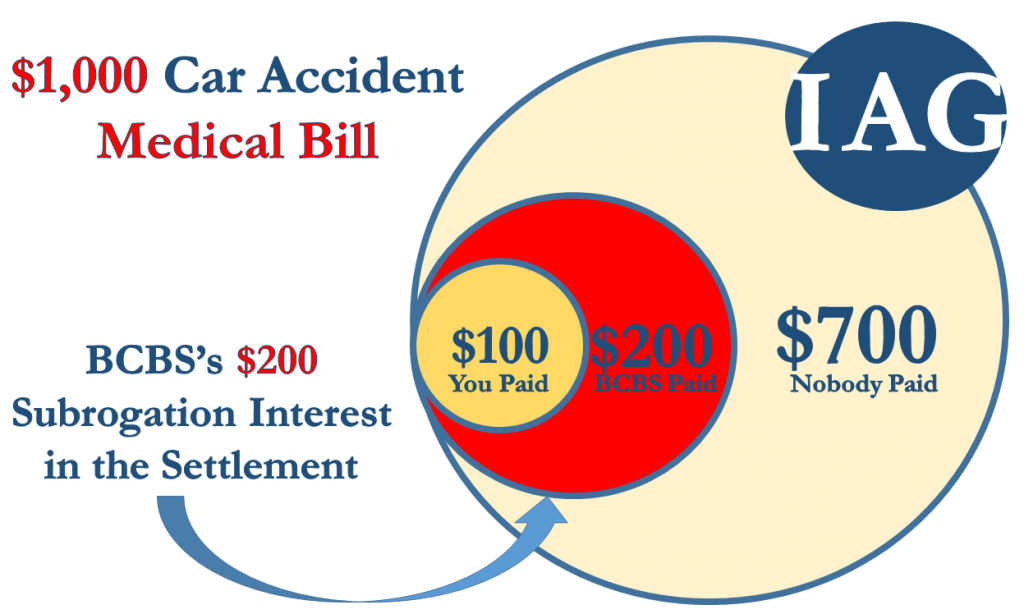

♦ John had Blue Cross Blue Shield (BCBS) health insurance

♦ John was rear ended in a car accident

♦ John had 1 doctor visit

♦ The doctor charged $1,000 for the visit

♦ BCBS negotiated that bill, with the doctor, down to $300

♦ John’s deductible / co-pay was $100, which he paid out of pocket

♦ BCBS paid the remaining $200

Let’s diagram that so you see how it looks:

Out of the $1,000 total medical bill, only $300 was actually ever paid ($100 by you and $200 by BCBS). The remaining $700 disappeared, nobody ever pays it.

2: Car Accident Medical Bills When There is Insurance

The above situation is how health insurance works in America. The health insurance companies strike deals with medical providers, who become part of that health insurance company’s “network.”

As a result, when you go to an “in network” doctor and pay with your health insurance, you pay a predetermined, negotiated price, not the “sticker price.”

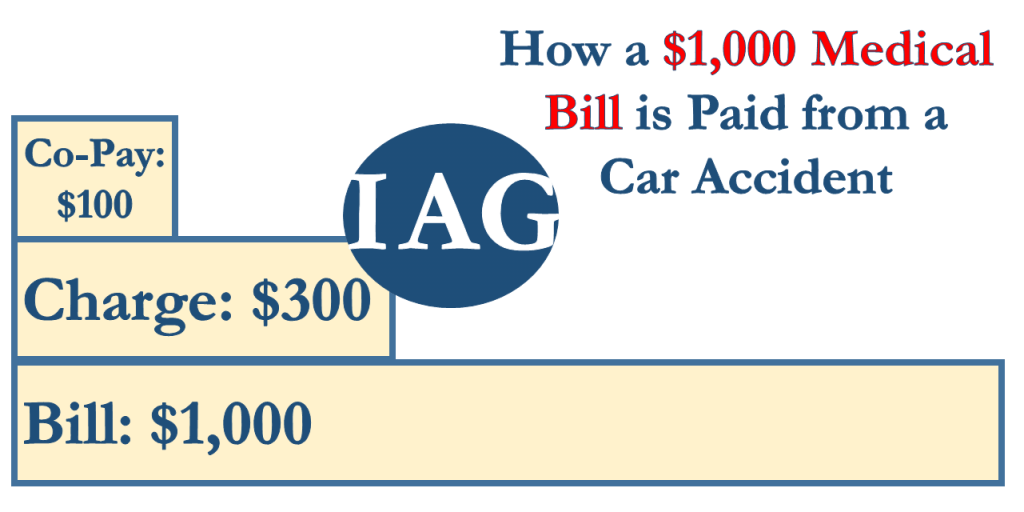

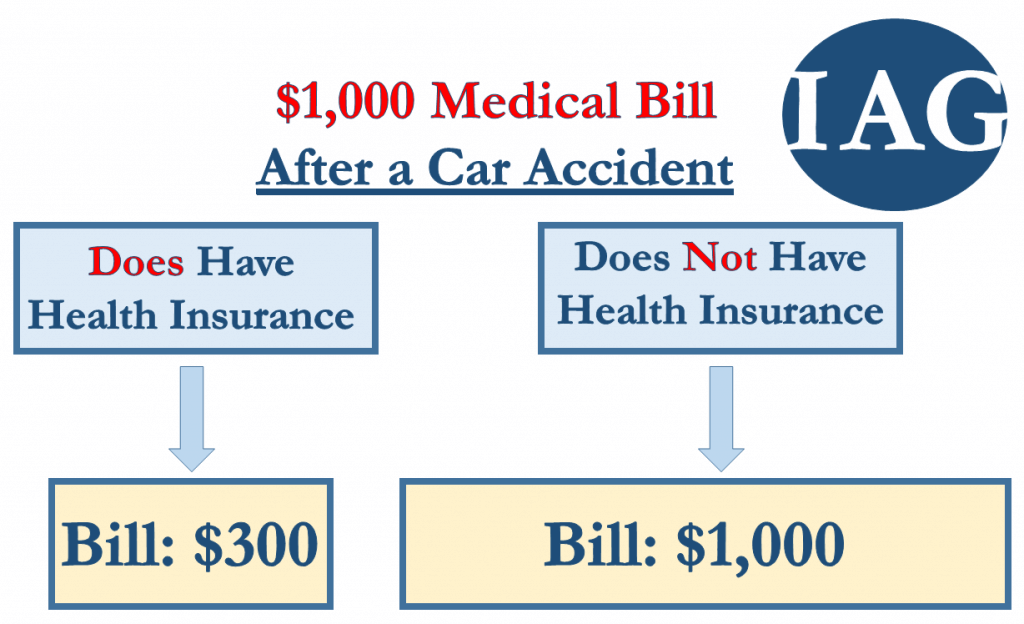

BUT, and this is a very important BUT in terms of you making money from your car accident settlement in states like California, you still get “billed” the sticker price ($1,000, using our example with John). Let me explain with another visual:

Sometimes that initial amount (the $1,000) is referred to as the “billed” amount, and sometimes it is referred to as the “charged” amount. What it is called is not important. What is important is that you understand there is a 1st layer and 2nd layer in terms of what the doctor wants to get paid. I will refer to that 1st layer or amount as the “bill” or “billed” amount for this article.

Some people think when you use health insurance to pay your car accident medical bills it works like this:

That is wrong. It does NOT work like that.

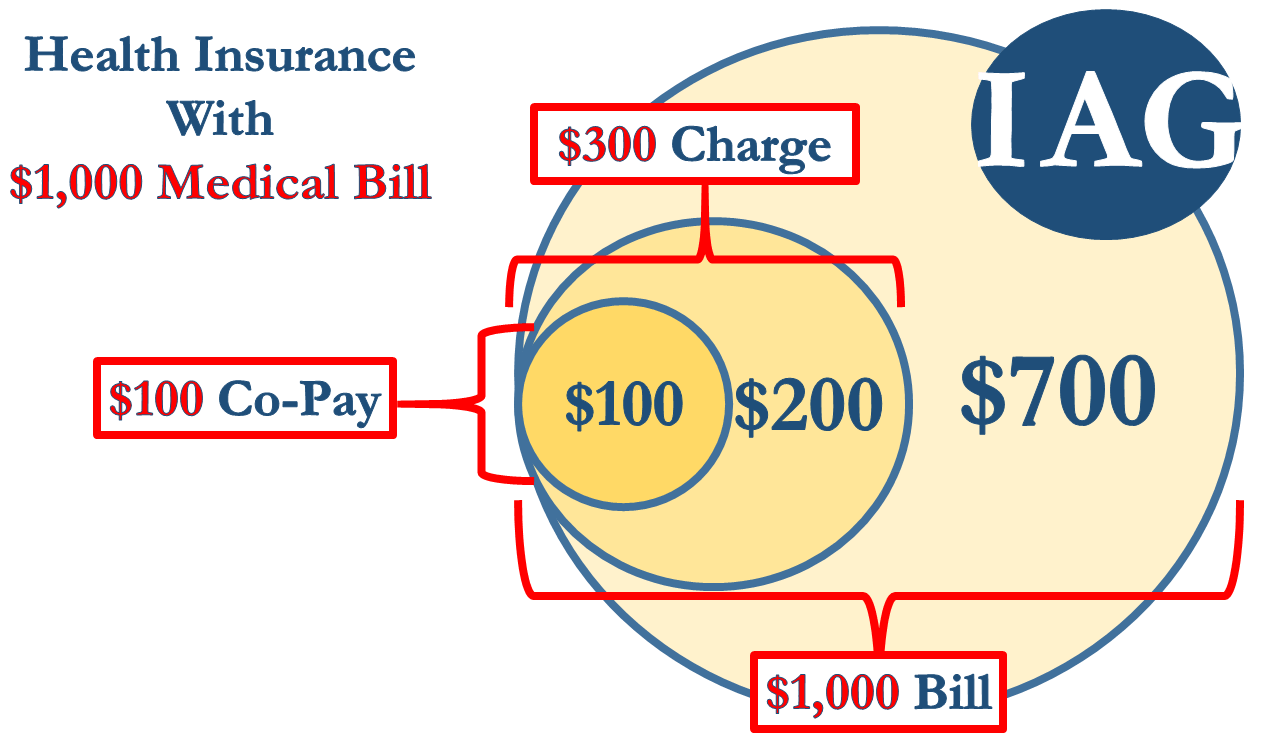

If you have ever dealt with medical bills for health insurance, you know this. Just look at the post-treatment bill you get from your insurance company, called an “EOB” (explanation of benefits).

Your EOBs, even if the medical bill is related to car accident treatment, shows that you got billed the sticker price ($1,000 in our example).

It then shows how much you were charged, as a result of your health insurance company’s negotiation with the medical provider ($300 in our example).

Lastly, it shows how much of that charge is your obligation, known as a co-pay or deductible ($100 in our example).

I will explain in a little bit how that impacts how much you have to pay of your medical bills and how that changes your net result (in a good way), but first a very quick introduction to subrogation rights.

3: Health Insurers Have Subrogation Rights on Your Car Accident Settlement

The technical definition of a subrogation right is not important. You need a plain English definition of what it means for you and your car accident settlement. Here it is.

Going back to our example of John and his $1,000 post-accident medical bill, John’s health insurer – Blue Cross Blue Shield (BCBS) – has a legal right to be paid back, from John’s settlement money, the $200 that it paid:

Why? Because BCBS is the one who paid that $200, not you!

In other words, the person who caused your accident and caused you to suffer lost wages, pain, suffering, and other losses, also caused BCBS to lose $200. Just like you have a right to get paid back for your losses, BCBS has a right to get paid back its losses, too.

Your attorney can negotiate the subrogated balance (discussed below), but your attorney cannot ignore it. Do not even ask. It is an easy way for a lawyer to get sued by a billion dollar insurance company.

Once your lawyer receives the settlement check, she or he has to write and send to BCBS a check to pay back the satisfy and resolve the subrogation interest.

4: Net Result of Who Pays How Much of Your Medical Bills After a Car Accident

Remember when I said above that it was a “very important” distinction that you still get “billed” the $1,000 sticker price? This is why:

HOW YOU MAKE MORE MONEY

Even thought nobody actually paid $700 of that $1,000 medical bill from your accident treatment, you can still recover that $700 from the other driver as part of your car accident settlement or verdict.

Here is a more realistic, and common, example to illustrate how powerful that can be:

– You have $100,000.00 in medical bills after your car accident from recuperative treatment.

– Your health insurance got that $100,000.00 negotiated, with the medical providers, down to $20,000.

– The result is $80,000 of those bills were never paid by anyone, they disappeared.

You can still get the other driver to pay $100,000 of your medical expenses after your accident, including the $80,000 that neither you nor your health insurance company ever paid for!

Now you understand why this is not just semantics. This is more money in your pocket.

You also know everything necessary to address the original question of, who pays your medical bills in a car accident?

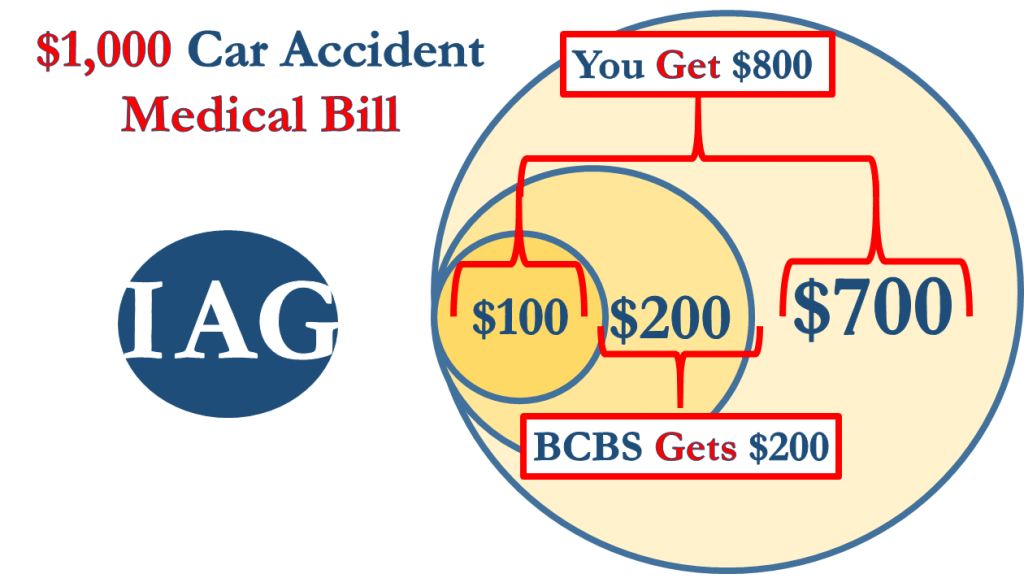

Using the $1,000 example we have discussing, if health insurance was involved, the answer is:

♦ First, BCBS pays the doctor $200

♦ Second, you pay the doctor $100

♦ Third, the negligent driver pays you $1,000

It looks like this, in terms of everyone who gets paid at the finish line:

This math is not final. To keep our math simple and not cause confusion, I did not include the following facts into the equation:

♦ Negotiated reduction of subrogation amounts

♦ Strategic reduction of co-pays and deductibles

♦ Attorneys’ fees from the settlement

♦ Reimbursed case expenses

The point was to teach, and answer the question of, who pays your medical bills after a car accident? Hopefully I accomplished that.

If you were involved in a car accident, used some form of health insurance to pay for your after accident medical expenses, and need legal advice regarding those medical bills or your treatment, my contact information is just a few scrolls below. You can reach out any day or time, 24/7.

If you already have an attorney who referred you to a doctor who is kind enough to be providing you medical care on a lien, continue to Chapter 2 to learn how the formula changes in those situations.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 2:

Medical Lien Calculation in Accident Claims

2 Paths, 1 Finish Line

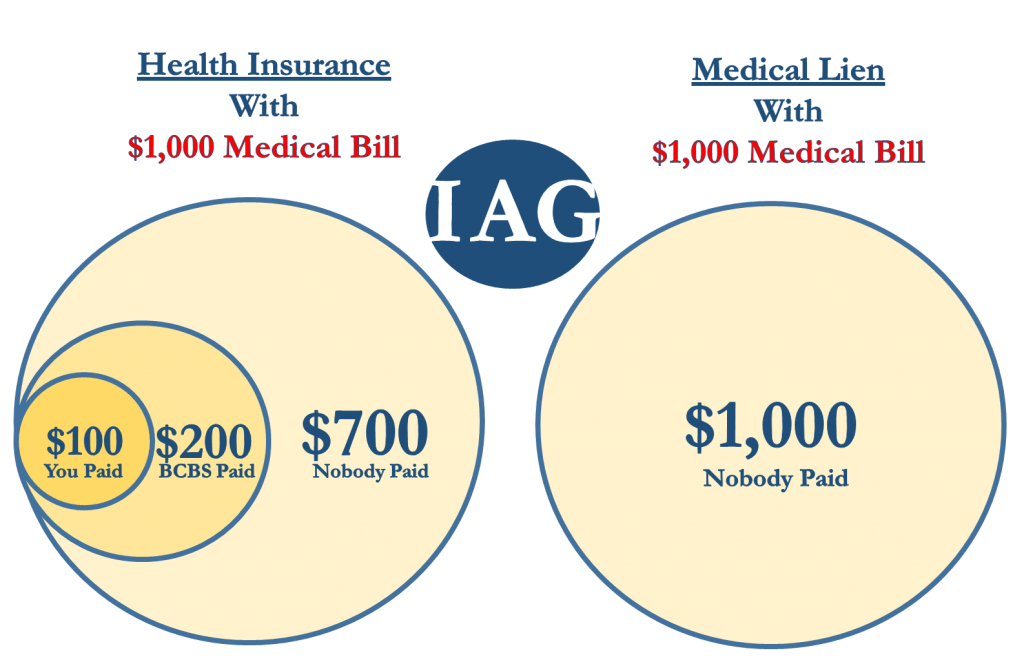

You learned in Chapter 1 that if you use health insurance to pay your car accident medical bills, the payment obligations, in a $1,000 hypothetical, may be distributed like this:

In this hypothetical, the doctor bills you for $1,000.

Your health insurance company gets that bill reduced to $300, which is the actual amount charged. Your health insurance company pays $200 of that $300 charge to the doctor.

The remaining $100 is your co-pay that you have to pay to the doctor.

In your settlement, you get to recover the full $1,000 bill, even though you only paid $100 out of pocket.

From that $1,000, you have to pay your health insurance company back the $200 of the $300 charge share that it paid.

You get to keep the remaining $800 ($1,000 – $200 = $800).

Because you had paid $100 out of pocket (your co-pay), that remaining $800 is really $700 of net recovery for you ($800 – $100 = $700).

If you got your treatment on a “lien”, you more or less reach the same result, but from a different path, which I will now outline for you.

What is a Medical Bill Paid by Lien?

You might end up with a medical lien for many reasons. Here are a few:

♦ You do not have health insurance

♦ Your health insurance only authorizes a certain number of treatments, which you already used up

♦ Your health insurance plan does not cover the specialists or treatment you need

♦ You cannot afford to pay 100% of your medical bills out of pocket

♦ You need a referral to see a specialist, it could take weeks or months to get that, but you are in pain and need a specialist now

If you end up in any of these situations, you could get the medical treatment you need in exchange for a lien.

Here is how a medical lien works:

♦ You are in a car accident and need medical treatment

♦ For one of many reasons, you do not have a source of payment for that treatment

♦ The doctor agrees to give you treatment in exchange for you signing a lien

♦ You sign the lien-document

♦ The lien assigns to the doctor a legal interest in your settlement

♦ When your case settles, the doctor gets paid for the treatment from your settlement

In short, the doctor takes care of you in exchange for a legal promise that you will pay the doctor back.

Why Do Doctors Offer

Medical Care On Liens?

The lien gives your doctor peace of mind. The doctor gives you the treatment on a lien without being paid because she or he knows that payment must be made from your settlement. Why “must”? Because that is what the lien document says. It is an absolute, non-revocable right.

The lien is so strong that your attorney cannot do any workaround to avoid paying it. If an attorney does not honor a medical lien, that attorney will be serious hot water. What I mean is, it is not an option to sign the lien and tell your lawyer to not pay it at the end of your case.

Sometimes clients ask attorneys to do that. The client asks that the attorney give the client all the money and the client will deal with the aftermath of the doctor chasing the client down for the money.

That is not an option. Your attorney will not, and cannot, distribute the doctor’s lien-encumbered portion of the settlement to you.

How Does a Lien Impact Your Settlement

The best way to explain this is to put the health insurance outcome side-by-side with the lien encumbered outcome. It looks like this, continuing with our $1,000 hypothetical:

You should understand now why the medical lien protecting the doctor is so strong. When the doctor accepts your health insurance, the doctor is guaranteed a certain payment from the health insurance company.

In contrast, when your doctor accepts the payment with a lien securing the future payment, the amount, if any, of that future payment is uncertain. Consequently, so too is the repayment to the doctor.

Who Pays a $1,000 Medical Bill That is

Encumbered by a Lien?

Let’s again put it side by side with the health insurance final outcome so you can see how it looks:

Four things to explain about this.

1: Why Does the Health Insurance Scenario Result in a $700 Net, not $800 Net?

First, you will recall that with health insurance you had a $100 co-payment. When you get the $1,000 settlement check, you will pay off your health insurance company’s $200 subrogation claim. Yes, you have $800 left ($1,000 – $200). However, you already paid $100 out of pocket earlier on for your co-pay. Thus, your net result is $700 ($1,000 – $200 – $100).

2: Why Does the Medical Lien Scenario Result in a $300 Net?

Second, you will see with a medical lien I calculated that, even though you owe the doctor $1,000, you still received $300. Why?

This is not set in stone, and it varies greatly, but it is fairly typical for doctor who provides medical care on a lien basis to offer the patient around 30% off of the total balance when collecting on that lien when the patient’s case settles.

Do NOT show a doctor this website and say, “look this is common practice.”

Sometimes 0% is taken off the total balance. Sometimes 50%.

There is a lot that goes into this, which I could write an entire book on. Remember, I am teaching general concepts to answer the question of who pays your medical bills after a car accident. To do the real math, you need a lawyer with experience negotiating lien balances.

3: Why Doesn’t the Medical Lien Doctor Give a Larger Reduction?

We discussed earlier that with health insurance the doctor has a guarantee of at least $200 of payment from the health insurance company, plus a fairly likely guarantee that you will pay your $100 co-payment. That’s $300 of guaranteed payment.

With a medical lien, there is zero guarantee. The doctor treating you on a lien is being very generous by taking a substantial risk that she or he may never get paid if your case does not turn out well. Because of that risk, the doctor gets more.

When you look at it through the doctor’s point of view, it makes more sense. The doctor accepting liens is not that much better off, especially considering the stress of the doctor not knowing when, if ever, she or he will get paid, and having to wait years for your case to resolve before finally get paid.

It might look something like this, in terms of the doctor’s bill collections:

4: Will You Net More By Using Health Insurance Instead of a Lien?

4(a): The Mathematical Answer

Using my hypothetical math and assumptions, you net $700 when health insurance pays your medical bills and $300 when you get your medical bills are covered through a medical lien. Assuming this is the real math in your case, does that mean you are better off having health insurance pay your medical bills rather than getting your medical care through a lien? No.

I made the following assumptions for our $1,000 medical bill, health insurance hypothetical:

♦ Health insurance will get that bill reduced down by 70% (which took the balance from $1,000 down to $300)

♦ Health insurance will pay 2/3 of the remaining balance (which made your out of pocket portion $100)

Those are very accurate assumptions and average scenarios. However, I have encountered cases where:

♦ $50,000 in medical bills resulted in a $43,000 health insurance subrogation claim (only a 14% reduction, not the 70% in our hypothetical)

♦ The client had an out-of-pocket deductible / co-pay that totaled over $5,000 (client would pay 100% of the $1,000 bill in our hypothetical)

♦ Health insurer only paid $100 of the remaining balance of $1,000 (only a 1/10 payment instead of a 2/3 payment from our hypothetical)

There are plenty of situations where you will get the short end of the stick when you use your health insurance.

Both health insurance and lien reductions and payouts have variability which makes the final outcome uncertain.

However, the variability is greater with health insurance than it is with medical care provided on a lien basis. Good law firms have relationships with the administrative offices of doctors who provide care on a lien basis. Those relationships result in a financial benefit to you.

4(b): The Non-Mathematical Answer

Some lawyers may disagree with my assessment above. Those lawyers say there is less variability in health insurance subrogation amounts and even if there isn’t, the negotiated rates are usually so low there is a greater net benefit, on average, by using health insurance instead of lien-treatment. Based on this, some of my colleagues advocate that health insurance should always be used if it is available.

I strongly disagree, because my fellow colleagues who take that position are overlooking something major.

When you get medical care through your health insurance, you have less control over who will be your doctor. If your case does not settle, your lawyer will need a doctor to testify in support the medical causation issues in your case. Many doctors refuse to become involved in litigation. If your doctor is one of those people, your attorney has only one choice. Your lawyer must retain a hired gun to testify for in your case.

Who do you think a jury will believe more, a hired gun or the impartial doctor whose only goal was to help you get better after your car accident?

The better witness is your treating doctor. Better witnesses result in better settlements and verdicts. Doctors who treat on liens are almost always willing to testify for their patients.

Thus, those lien-treating doctors open the door for you to recover more, offsetting potential differences in that doctor’s larger medical lien versus what would have been a potentially smaller insurance subrogation interest.

4(c): It is Complicated

As you can tell, this gets very complicated. This is part of what a good motor vehicle accident lawyer does for you.

A good lawyer keeps an eye on your liens and bills as your case, and medical treatment, progresses. They will keep you in the loop, and together you will make decisions about how to position your case to ensure you get have the best evidence lined up, and get the most money possible when you cross the finish line.

The other thing a lawyer does for you is manage the repayment of your liens and health insurance subrogation claims. That is the subject of Chapter 3, coming up next.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 3:

Payment of Subrogated Accident Medical Liens

Payment of Health Insurance Balances

From Car Accident Medical Bills

Two Parts of Your Medical Bill Must Be Paid

I will stick to the $1,000 hypothetical to explain this. To refresh your memory, when you used your health insurance to pay your medical bill after your accident, it looked like this:

The two parts that must be paid are:

♦ $200 subrogation interest

♦ $100 co-pay / deductible

I will discuss the subrogation first.

Payment of Medical Bill Subrogation From Car Accident

Your health insurance company only gets to enforce its subrogation rights against a recovery, whether that recovery is from a settlement or a verdict. If you decide to not pursue your car accident case, or you lose your case, there is no recovery. Therefore, if you lose your case or do not pursue one, there is no subrogated claim that you have to pay.

If you do pursue your auto accident claim and do recover a settlement or verdict, you have to pay back your health insurance company’s subrogated claim from that recovery.

Thankfully, health insurance company’s are very familiar with this process. They often assign their right to pursue the subrogation to a third-party, such as The Rawlings Group.

Whether it’s the health insurance company directly or a third-party subrogation company, they will wait patiently for your case to resolve. They will not, and cannot, send you to collections before that. Until you reach a settlement or verdict, you technically do not owe them a penny.

Because of this, the health insurance company’s subrogated interest is not something to worry about. Let your lawyer deal with the headache of their constant follow-up e-mails, phone calls, and letters. When the case resolves, your lawyer will negotiate and pay off the subrogation claim from the settlement.

Payment of Medical Bill Co-Pays From Car Accident

The co-payments and deductibles are trickier.

That $100 portion of the medical bill that we have been talking about is a real bill. It is not contingent on your settlement or verdict, or you pursuing a case. You have to pay it when it is due. If you do not pay it timely, the doctor or hospital that you owe that bill to can send you to collections.

This is hit or miss. Some doctors and hospitals will wait it out patiently for your claim to resolve so long as your lawyer keeps the medical provider updated regularly with assurances that the bill will be paid from your recovery. Some medical providers will send you to collections even when your lawyer provides those assurances.

This can be a big problem if:

♦ You need surgery

♦ You have a larger deductible

♦ Your treatment takes place over several calendar years, resulting in multiple yearly out-of-pocket maxes being stacked on top of each other

Any of these scenarios could result in you having $10,000 or more in medical bills that you have to pay.

There is no typical formula or approach for this. You need to speak with a lawyer about your specific case, treatment timeline, balances, and potential settlement timeline. Sometimes I can dangle a carrot in front of the doctor or hospital to get them to hold off from submitting your bill to collections just long enough for the case to settle.

If you are in this situation, call my office and ask to speak with one of our lawyers. We will do our best to dig you out of that hole, or if it’s not too late, prevent you from falling into it in the first place.

Payment of Medical Liens

From Car Accident Medical Bills

If your outstanding balance is on a medical lien, you are in a similar situation as you would be with a subrogation claim by a health insurance company in terms of timing of payment. A doctor who extends on offer to treat you on a lien is aware that she or he will not get paid until you get your settlement or verdict.

For that reason, the medical provider will be patient and not send you to collections, and these are balances that you should not worry about during the pendency of your claim.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 4:

Medical Lien & Subrogation Reduction Techniques

3 Techniques to Reduce or Eliminate

Your Medical Lien & Subrogation Balance

Technique #1: Negotiations

If you have a medical bill balance that needs to be paid back from a car accident, your lawyer can negotiate with the bill holder to reduce that balance.

This can be done for liens, direct balances resulting from co-pays with a provider, and health insurance subrogation balances. Much of the success in these reductions comes from relationship building, and skilled negotiation.

It helps when the Rawlings adjuster recognizes the person on the other line, and is willing to extend her full reduction authority as a result.

The same is true of doctors who work on liens. Those doctors have billing departments. The staff who run those billing departments become friendly with the lawyers and paralegals they have worked with before. If a big reduction is needed to help you make more money in your case, the lawyer can sometimes call in a favor to get that done.

This is the simplest, and most straightforward way a lawyer can reduce your medical bill balance.

Technique #2: Collection Gamble

The second technique comes with a disclaimer that you should not even consider trying it without speaking a lawyer, as a starting point. You may need to speak with a financial planner, too.

I’ll use a hypothetical to illustrate this technique:

♦ John used private health insurance to pay for his medical bills after a car accident

♦ John’s health insurance policy has a high out of pocket max for the year of $5,500

♦ John’s car accident happened in October of 2015

♦ John received medical care for his car accident injuries from October 2015 through March 2017

These facts are not that uncommon. Health insurance is expensive. A lot of people purchase small premium policies to protect them from catastrophic events. Those small premium policies often have large out-of-pocket maximums for a calendar year.

These facts are also the perfect storm. Because John’s accident happened in October, he is likely to cap out his $5,500 out of pocket max for 2015. He will do the same for 2016 and 2017, for another $11,000. He now owes an out-of-pocket balance of $16,500.

Depending on a host of variables, including an uncompromising medical provider who won’t reduce that balance for John, a situation could arise where John could net close to $0 from his settlement after deductions for attorneys’ fees, case costs, and the $16,500 he paid out of pocket.

Faced with this dilemma, John might roll the dice and let those bills go into collections.

Why? Because once the bill is sent to collections, an opportunity arises for substantial reductions to be negotiated with the collection agency. Notice I used the word “opportunity.” There is no guarantee here. But sometimes, these balances can be settled for 20 cents on the dollar or less.

Unlike medical liens or subrogation interests, your lawyer has no obligation to force you to pay back your co-pay balance. That is why this technique is an option for your health insurance co-pay and deductible balance, but not for medical liens or subrogated balances.

I reiterate that I am not advising anyone try this approach without getting professional advice. It can negatively impact your credit, and it’s a very situational strategy. I have only encountered a handful of times where it made sense for a client to utilize this technique.

Technique #3: The Truth Hurts

This is by far the most complicated of the 3 techniques I am revealing in this article. It is not something you can pull off without a lawyer, because to set it up a skilled lawyer needs to calculate how much your case is potentially worth very early on, and then make a few strategic maneuvers to leave the door open for the technique to succeed.

Assuming those preliminary steps have been properly set up, I will use a hypothetical to explain how and when the technique works and could be used:

♦ You injured your back and neck in a car accident

♦ You used your health insurance to pay for the medical bills, which total $30,000

♦ From those bills, your health insurer has a $10,000 subrogation claim

♦ $5,000 of that subrogated interest relates to medical bills and treatment for your back

♦ $5,000 of that subrogated interest relates to medical bills and treatment for your neck

♦ Your lawyer submits a settlement demand

♦ The defendant’s car insurance company makes a low offer, because they say all your back problems are pre-existing

For a variety of reasons, you might want to settle your case right now. You might be strapped for cash. You might not have the stomach for protracted litigation. You might want to move on with your life and get the case over with, even if the settlement amount is not fair, as long as you get something.

Here is how your lawyer can accomplish that (again, assuming it has been set up properly in advance), and why I call this method “The Truth Hurts.”

Whatever letter, IME report, email, or other documentation the insurance adjuster sent your lawyer is important for this. In that document, the insurance adjuster is claiming that no settlement money will be paid for your back injury because your back problems are pre-existing.

Your lawyer forwards that letter to the subrogation carrier with a cover letter. That cover letter explains why the $5,000 subrogation claim for medical bills related to your back should be cancelled.

Why? Because the subrogation claim only attaches to medical bills you incurred from the accident. If you incurred medical bills for back treatment, and the back injury was pre-existing and not related to the accident, the insurance should not get that $5,000 for back treatment from your car accident settlement.

Could this technique help you pocket an extra $5,000 from your settlement? Maybe. A lawyer on our team used this technique to put over $20,000 into a client’s pocket for a very difficult case. Call our office for a free consultation, and we can figure out the best path forward for you.

Call or Message Us 24/7

(800) 484-0779

Your

Los Angeles Motor Vehicle Accident Attorney

Click or Tap for a Free Consultation

Chapter 5:

Q&A On Accident Medical Bills & Payments

Q&A on Accident Medical Bills

Will Health Insurance Cover My Car Accident Injuries?

Yes, your health insurance will cover your car accident injuries. As explained above, after your health insurance covers your car accident injuries by paying those medical bills, your carrier will have subrogation rights. Through those rights, they can recover from your settlement the amounts they paid towards your car accident injuries.

The other issue is, although your health insurance may cover your car accident injuries, you health plan may not provide optimal treatment options. It may also provide limited treatment options, or cut off your treatment when you are still injured. If you are in any of these situations, you should call a lawyer immediately before you have what the car insurance company’s call a “gap” in treatment, which will be used as justification to give you a lowball offer.

Injured in a Car Accident With No Health Insurance

If you were injured in a car accident with no health insurance, do not worry. Call the Injury Advocates Group, and we will refer you to a network of specialized accident care providers who will treat you on a lien basis. That means the doctors will hold your bill until the case resolves. They will not send you to collections, and they will not haggle and harass you for payment during the months or years that your case is pending.

Even if you have health insurance and were injured in a car accident, getting treatment on a lien basis may be the best decision for you. This could be true, for example, if you have limited in-network providers, or your in-network providers are booked for weeks or months out. If you have to wait a week or more for an appointment, that could substantially damage the value of your case.

The point here is, you have options if you are suffering from car accident injuries and have no health insurance. The key is that you act fast to get treatment before the insurance company gets to argue that you have delayed treatment which suggests you were not hurt badly.

Do I Have to Pay Medical Bills From My Settlement?

Yes and no, you may have to pay the medical bills from your settlement. If you read the article above you understand why the answer cannot be a clean “yes” or “no”. Some portions of your medical bills may be waived entirely. For those portions, you do not have to pay them from your settlement. Other parts will be encumbered by a medical lien or subrogation rights. Those portions of your medical bills you have to pay from your settlement.

With the above explanation in mind, the simplest possible answer is this: Yes, you will have to pay at least some portion of your medical bills from your settlement, but the specific portion that you will have to pay will vary greatly depending on the type of treatment, who paid for it, and what reductions your lawyer can obtain for you.

Is Negotiating Medical Bills After Settlement An Option?

Yes, negotiating medical bills after your settlement is an option. I would say it is more than an option. Negotiating your medical bills after a settlement is something that Injury Advocates Group does as a courtesy for all clients. It should almost always be done.

Why “almost always”? Sometimes, depending on the type of lien or subrogation right and the settlement amount, no medical bill reductions are available. In those circumstances, you could spend weeks or months trying to get a discount when it just will not happen. A good lawyer can issue spot those situations ahead of time. That will help you get your settlement payout weeks or months sooner without chasing a dead-end.

In other situations, negotiating your medical bills after a settlement is a bad idea, and you should do it before the settlement. That sometimes gives you more leverage with the medical provider, whereas your negotiation leverage may be reduced if you first accept a settlement.

What if My Medical Bills Exceed Policy Limits?

If your medical bills exceed policy limits, your case is not lost, but you should call a lawyer ASAP. There are some creative solutions that could help in these situations, but they are fairly complicated and apply to a narrow set of situations.

When the medical bills exceed the available policy limits and none of the creative solutions can help you, you have to try one of two basic options. The first option is negotiating the medical bills. The second option is searching for more insurance coverage. Maybe there is a negligent road design case? Maybe a viable negligent entrustment count exists which would trigger an additional policy? Perhaps a resident relative exists that has a larger policy that can be pierced?

This is not one of those try it yourself situations. If the total of your medical bills exceed the policy limits, call an experienced lawyer before you accept any policy limits offer. There may be more there than meets the eye, or what the insurance adjuster is sharing with you.

Does Medicaid Cover Car Accident Injuries

Yes, Medicaid covers car accident injuries and will pay the medical bills caused by your car accident. Although Medicaid covers car accident injuries, there are two downsides to that payment that should be considered.

First, when Medicaid covers any third-party liability, such as car accident injuries, it will have a statutory right of recovery from your settlement. That is, in practice, the same as a health insurance subrogation right. The major difference is that Medicaid is fairly bullish about negotiating. Do not expect any major reductions from Medicaid either before or after your settlement.

Second, when Medicaid pays for your car accident injuries it does so at Medicaid’s reimbursement rate. That means a $1,000 medical bill may become a $300 medical bill. This can be good or bad, depending on a variety of factors. For example, if you case is with State Farm and you want an early settlement, this will be bad because State Farm will argue Medicaid’s reimbursement rate represents the true value of the treatment.

Does Medicare Cover Car Accident Injuries

Yes, Medicare does cover car accident injuries. Everything explained above about Medicaid applies equally to Medicare. There are issues with reimbursement amounts and liens that can hurt your case, and Medicare is very bullish about negotiating any discounts. That said, our lawyers have had success getting Medicare liens reduced by as much as 50%.

If Medicare covered some or all of the medical bills related to your car accident injuries, call our office. You need a closely monitored game plan to ensure the Medicare lien does not gobble up your settlement or hurt you more than its low negotiated payment rate helps you.

The Finish Line

Who Will Pay Your Medical Bills

After a Car Accident?

Summation

I want to end where we started, with the two questions that brought you here:

The first question is, who pays your medical bills after a car accident?

The second question is, who should pay your medical bills after a car accident?

The combined, and complete, answer is this:

After a car accident, you and your health insurance carrier pays your post-accident medical bills. Who pays how much will depend on your specific health insurance policy.

If you do not have health insurance, you can get medical care by signing a lien with a doctor who will agree to wait for your case to settle before receiving payment.

Regardless of which option you take, you can recover the full face value of your medical bills from the driver that hit you, or that driver’s insurance company, depending on the state you live in (different states have different rules for this).

Regardless of whether you used a medical lien or health insurance, someone – either a medical provider or a health insurance company – will have the right to take from your settlement the portion of your medical expenses they paid. Your lawyer can negotiate with all of these entities to reduce how much is paid back.

Los Angeles Personal Injury Lawyers

If you were in a car accident, are racking up medical bills, and are wondering who will pay for them, how much of them you will have to pay, or whether you will make any money in your settlement based on the trajectory of your treatment, liens, bills or overall claim, I invite you to call us.

Our law office is based in Los Angeles, but we can help even if you are not in Los Angeles City or County.

You can call me 24/7 at (800) 484-0779, e-mail me at info@injuryag.com, or fill out the contact form below.

About the Author

Article Author: This law article was written by attorney Ray Benyamin, Esquire. Mr. Benyamin received his Juris Doctor degree from the Thomas Jefferson School of Law, and his license to practice law from the State Bar of California. His law license number is 277263. He has been practicing law for 10 years. Mr. Benyamin is a registered member of the following legal organizations: Consumer Attorneys Association of Los Angeles (CAALA), the Los Angeles County Bar Association (LACBA), the State Bar of California, the American Bar Association (ABA), and the American Association for Justice (AAJ). Mr. Benyamin has personally helped his clients recover over $10,000,000 dollars in vehicle accident insurance claims in the State of California.

![]()

Our Lawyers Serve Clients in Los Angeles, California & Nationally

Serving all of Los Angeles, including Arcadia, Beverly Hills, Claremont, Canoga Park, Chino, Chino Hills, Covina, Diamond Bar, Downey, East Pasadena, El Monte, Encino, Highland Park, Inglewood, La Verne, Long Beach, Malibu, Montebello, Monterey Park, North Hollywood, Northridge, Pasadena, Pomona, Rancho Cucamonga, Reseda, Rosemead, San Gabriel, San Dimas, Santa Monica, Sherman Oaks, South Bay, South LA, South Pasadena, Sunland, Tarzana, Thousand Oaks, Torrance, Van Nuys, Venice, West Covina, West Hollywood, and Westlake Village.

Serving all of California, with a focus on Kern County, Los Angeles County, Orange County, Riverside County, San Bernardino County, San Diego County, Santa Barbara County, and Ventura County.

Serving nationwide in all 50 states on a case-by-case basis with a national network of relationships and on a Pro Hac Vice basis.